Understanding China’s Oncology Care: What Primary Research Reveals Beyond Secondary Data

Insights from groupH’s physician network across China – uncovering what truly drives patient and physician behaviour in oncology.

Insights from groupH’s physician network across China – uncovering what truly drives patient and physician behaviour in oncology.

Forecasting Reporting Approaches Document

For commercial analysis, get in touch: Erik Holzinger. Founder, groupH

erik.holzinger@grouph.com

I was delighted to attend the half-day Citeline Elevate Commercial event, focused on the pharma and bioindustry commercial landscape. It combined fireside chats, data insights and case studies in an intimate Whitehall setting in central London.

Here are my 5 key-take aways:

For commercial analysis, get in touch

Erik Holzinger. Founder, groupH

erik.holzinger@grouph.com

In October 2024, I attended and moderated a panel session at the New Product Planning (NPP) Summit in Boston. The NPP Summit is a gathering of biopharma and pharma professionals focusing on commercial and other NPP topics with lots of insightful presentations, networking, small group discussions, case studies and learning from others.

Here are my 5 key takeaways from the event:

1. You can’t afford to make any mistakes but if so, fail early

There is always a statement from a speaker that seems to stick in the mind even long after the event. Against the backdrop of another year of lacklustre investment in the biopharma industry and IRA forcing many companies to rethink their pipelines and programmes, for me this year, the statement was: ‘Failure is not an option’ from Steven Bloom, VinceRx. While not new, it sums up the current general mood and highlights an urgent call for action: To get even better at every aspect of what we are doing. Allowing to ‘Fail a programme early’ for commercial reasons is still not practiced enough for lack of commercial insight in the early stages of asset development.

2. The fallout from IRA so far, -13% for Part D drugs net but ‘on average’

IRA: While most presentations and panels covered this topic, there is still uncertainty about how this will play out in detail. The challenge IRA poses can seem somewhat overstated, while for individual products it can be substantial. ~80 Part B and Part D drugs will be subject to mandatory maximum fair price rebate negotiations by 2030. However, analysis of the first 10 drugs subject to rebate negotiations shows that the net impact, on average, is approx. -13% after IRA vs. rebates, and this is applicable only to the Part D portion of the payer mix. So, whether IRA will affect you or not will be on a case-by-case analysis.

3. AI: Too fast too soon – is it the end of the honeymoon period?

AI: Comments such as ‘too fast too soon’ echoed through some of the icebreaker exercises. Others referenced AI as the silver bullet that will help the industry to get better at what it is doing. The truth lies probably somewhere in the middle and, notably, as is often the case with AI, it is not always clear if we talk about AI in drug discovery and disease diagnosis or AI and machine learning in analytics and market research or even genAI and LLMs.

4. The traditional LCM model is dead

Another thread that weaved itself through many panels covering TPP development, commercial strategy, pricing and HEOR was the call for more commercial insight and identification of critical value elements earlier in the drug development process together with the courage, if needed, to fail early. The (early) NPP voice is critical for this job and, making sure that it comes across loud enough. And, leveraging multi-indication potential in post-IRA times requires close and early collaboration between NPP and R&D teams. In this sense the traditional LCM model is changing.

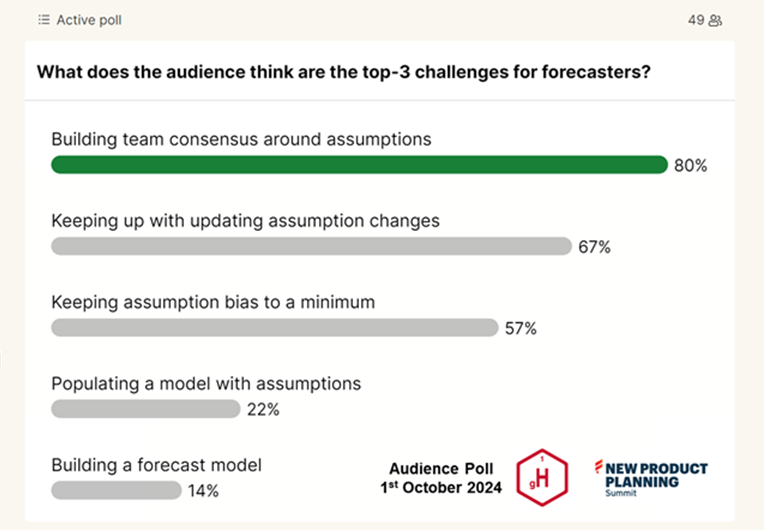

5. Forecasting: Building consensus around assumptions is the hardest part

As the LCM model is changing in line with shorter ROI times and potential price pressure from IRA, forecasting processes need to adapt. It was concluded that consensus building around assumptions is the hardest part. The forecasting process is not static and finding the right update frequency, the right tools or platforms is very much driven by individual market characteristics, the stage of the programme and the size of the organisation. While the future of long-term strategic forecasting may one day be algorithm/AI based with much less PMR input, the present reality is that this future is not yet there and that forecast structure and transparency and human factors of how it is being delivered to senior management play a far greater role in the success of a programme than any forecasting tool.

Get in touch

Erik Holzinger. CEO, groupH

erik.holzinger@grouph.com

Collective learning has been the main focus of this NPP Summit and how to best navigate IRA and leveraging AI during challenging times for biotech. On the topic of advanced forecasting this fantastic cross-industry panel shared their experiences on what panel and audience agreed was the main challenge: Managing the forecasting process and building team consensus around forecasting assumptions. Few were surprised that processes alignment with lifecycle and business needs play an important role but that, beyond this, unfortunately, there is no one-size-fits-all solution, only continuous evolution or well planned, customised step-change. Thanks to a very engaged and super-prepared panel, Ashley Robinson/BioMarin, Deepak Wadhwa/AZ, Aaron Furtado/Bayer and Mayank Misra/Soleno with Erik Holzinger/groupH moderating.

groupH’s discussion on TPP Development and Indication Prioritization took place at the NPP Summit Boston on October 16, 2023.

Erik Holzinger and Iain Clark talked through 2 project case studies focusing on pre-clinical or early-stage clinical stage by sharing client views on project timing and project learnings.

Please click on the here to view document.

NPP Summit_TPP Development and Indication Prioritization PDF

groupH has analysed what is known about the Inflation Reduction Act (IRA) of 2022, which constitutes a major legislative effort to address drug pricing and Medicare expenditure. We developed a simple easy-to-use model, which assesses the risk of any of the three parts of the IRA applying to a product that is either already on the market or still in development.

The IRA model has been developed based on primary market research with senior US market access experts and secondary analysis. The model and its associated white paper was first presented during the Fierce Biotech NPP Summit in Boston in October 2023.

Please click here to access the paper.

Please click on the image below to access the model.

![]()

Realistic net-prices and peak-patient-shares are key requirements for providing early commercial direction for assets whose clinical profile might not yet been finalised. Early to mid-stage commercial decision-making benefits from specialised tools that have been specifically developed for this purpose.

During the past year groupH developed an evidence-based Peak-Patient-Share tool (a.k.a. the Devil’s Advocate Tool) that was presented at the ephmra (European Pharmaceutical Market Research Association) Conference 2022.

The tool is now available and free-to-use on groupH’s website:

The requirement for the tool and its methodology is described in a comprehensive and downloadable guide document – groupH ephmra Paper

Please contact us for any questions, clarifications or for a customised tutorial or webinar.

5 mins video summary on Devil’s Advocate Tool

The North American Neuro-Ophthalmology Society’s (NANOS) 48th Annual Meeting took place on February 12-17, 2022 in Austin, Texas

In collaboration with Cambridge University and Gensight Biologics, groupH published a poster at the conference based on the findings of a qualitative study to explore the impact of Leber Hereditary Optic Neuropathy (LHON) on patients’ and their relatives’ lives. LHON is a rare condition which leads to blindness and disability in teens and young adults.

Please click on the image to view the poster

groupH has developed a simple US gross-to-net discount model including a proof-of-concept validation. This simple tool estimates applicable gross-to-net contracting discounts in the context of early-stage commercial assessments in the US market. The model has been developed based on in-depth primary market research with senior payers and secondary analysis. This paper was first presented during the EphMRA annual conference in June 2021.

Please click on the image below to access the paper

![]()

![]()

![]()